Three trends defining private market investing

Capital concentration: the limits of scale

With constrained deal markets weighing on both liquidity and fundraising, investors are deploying capital more selectively, prioritizing scale as a proxy for safety and concentrating commitments with the largest managers and strategies. In the first half of 2025, 42% of global private capital fundraising went to funds targeting $5 billion or more—despite these megafunds representing less than 4% of all strategies. Additionally, nearly all new capital flowed to experienced managers. While experience remains valuable in today’s uncertain environment, size is far from a reliable predictor of success. This is particularly true in private equity, where middle market funds have consistently outperformed their megafund peers. As capital continues to pool into the largest strategies across both institutional and private wealth channels, competition intensifies and return dispersion narrows. Scale may offer certain advantages—but in today’s market, alpha is more likely found in less crowded corners of the private capital landscape.1

Market share of annual global private capital fundraising*

* Includes private equity, private credit, and real estate fundraising. Experienced managers are those raising their 5th fund or later in that asset class.

Rate normalization: transforming the landscape

The 2010–2021 period was an interest rate anomaly. Higher financing costs are now a structural feature of the investment landscape, compressing equity returns and transferring value to lenders. This shift boosts the long-term appeal of debt strategies—but also increases risk, as lower debt service coverage ratios raise the stakes for credit investors. In equity strategies (both corporate and real estate), higher rates limit the return potential from leverage and valuation expansion. That places a premium on managers who can drive performance through income and earnings growth—via pricing power, operating efficiency, and margin expansion. The next cycle of alpha in private markets will be led by operators, not financial engineers.

Higher financing costs limit valuation upside

Geopolitical and policy volatility: investing through uncertainty

Policy uncertainty and macro risks have become central to the deal landscape. The new U.S. administration has pursued a policy agenda that sharply diverges from the prior three decades of relative stability. As we explore in our recent white paper, U.S. exceptionalism: At a crossroad, we firmly believe the U.S. remains the most dynamic destination for capital. But with transformational shifts underway in trade policy, geopolitics, and technology, uncertainty is the new normal. Investing through this volatile environment will require rigorous underwriting, expansive due diligence, and deep networks to source opportunities created by policy realignment and complexity.

Policy uncertainty is hindering the M&A recovery

Middle market macro view

In an era of rampant speculation and short-termism in public markets, the long-term focus of private investors is a real competitive advantage. As the market grows and expands, it is more critical than ever that investors home in on the segments, strategies, and managers that can drive alpha in this new era.

Private equity: The end of easy

Private equity investors entered 2025 with renewed optimism for a rebound in deal activity. But as is often the case in markets, macro conditions had other plans. What many anticipated would be a clear-cut, pro-business, deregulatory U.S. policy regime has turned out to be far more complex. Tariff policy has in particular disrupted the momentum that gradually returned in 2024—dampening growth expectations, keeping interest rates elevated, and, most consequentially, injecting uncertainty into investor sentiment. A tepid pace of realizations remains the rust clogging the industry’s flywheel—stalling capital recycling, stretching deployment timelines and disrupting fundraising cycles.

We are optimistic that deal flow will improve in the back half of the year. But there are larger, more secular shifts at play. What worked for PE managers in the era of low interest rates, persistent multiple expansion and placid globalization, will no longer suffice. The cyclical challenges of the past few years have exposed and accelerated the structural underpinnings of a new investment regime. Returns will need to be earned, not engineered. Investors who recognize the implications of these changes will be best positioned to capture the evolving opportunity in private equity—which we believe remains mission critical in an era of subdued return expectations for public equities.

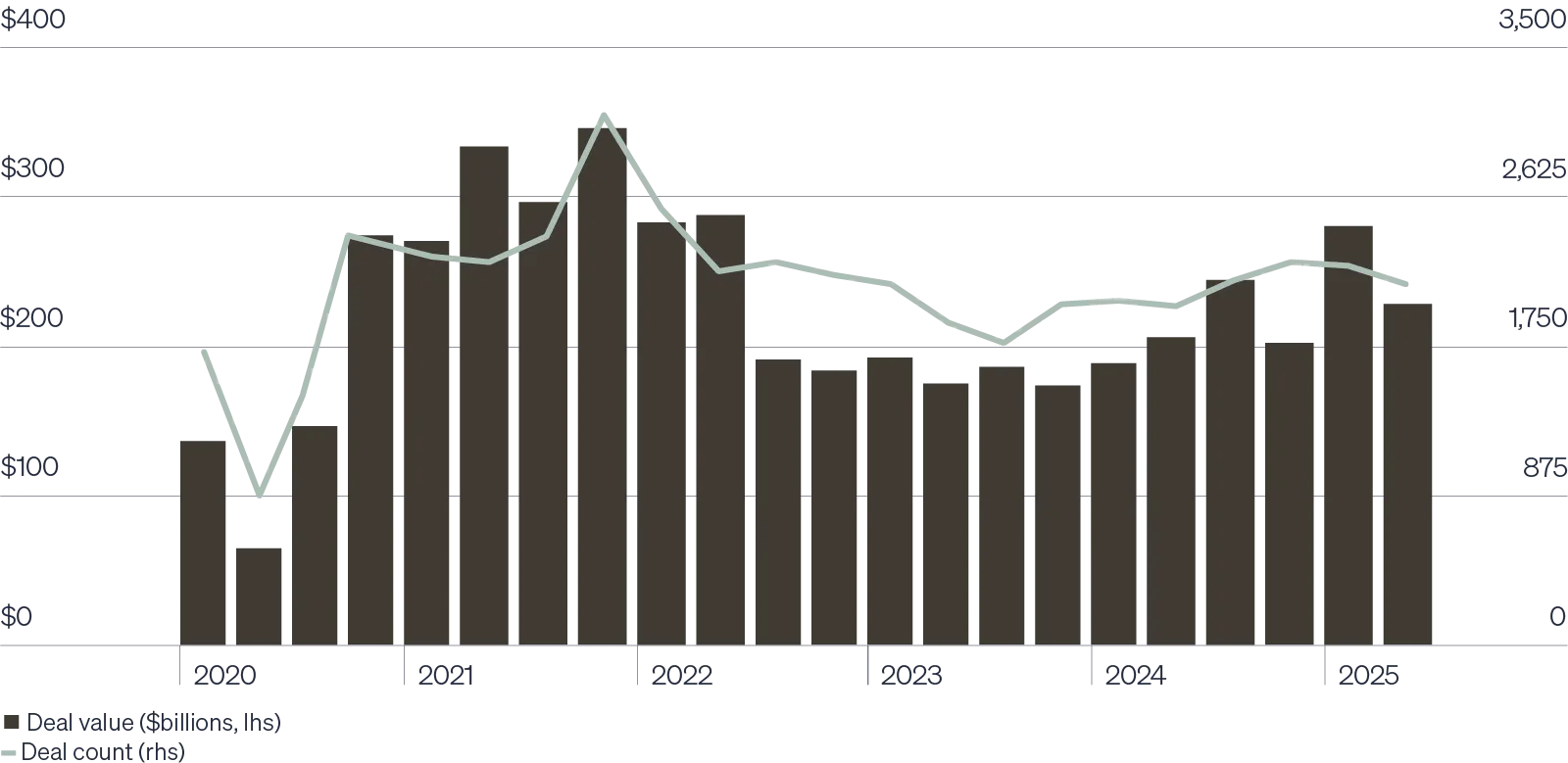

U.S. private equity deal value ($B) vs. count*

*Includes confirmed and estimated deal activity.

Private credit: The period of specialization

Private credit appears poised to enter a new growth phase, “The Period of Specialization.” The asset class has grown from strength to strength, building upon its value proposition while capturing market share. With the upper-end of corporate direct lending showing signs of maturity, we think investors should ask more of their private credit allocation. We identify specialized and emerging strategies offering better value and enhanced diversification—areas we think should lead the next phase of growth for private credit.

Although M&A activity is still uneven, direct lending continues to represent the primary debt provider for companies looking to finance growth and an attractive option for investors. The strategy has continued to perform consistently, returning 10.37% for the year ended March 31. This outpaced the strategy’s performance since inception (9.54%) despite new issue spreads tightening over the past year. Strong top line growth for U.S. middle market firms of 12.1% in 2024 kept credit losses well-contained and helped improve credit fundamentals throughout the period. The direct lending default rate has fallen each of the last three quarters, pointing to resilient borrower health. Private credit is durably more attractive in an era of higher rates, but with interest costs for borrowers elevated, manager selection will be critically important.

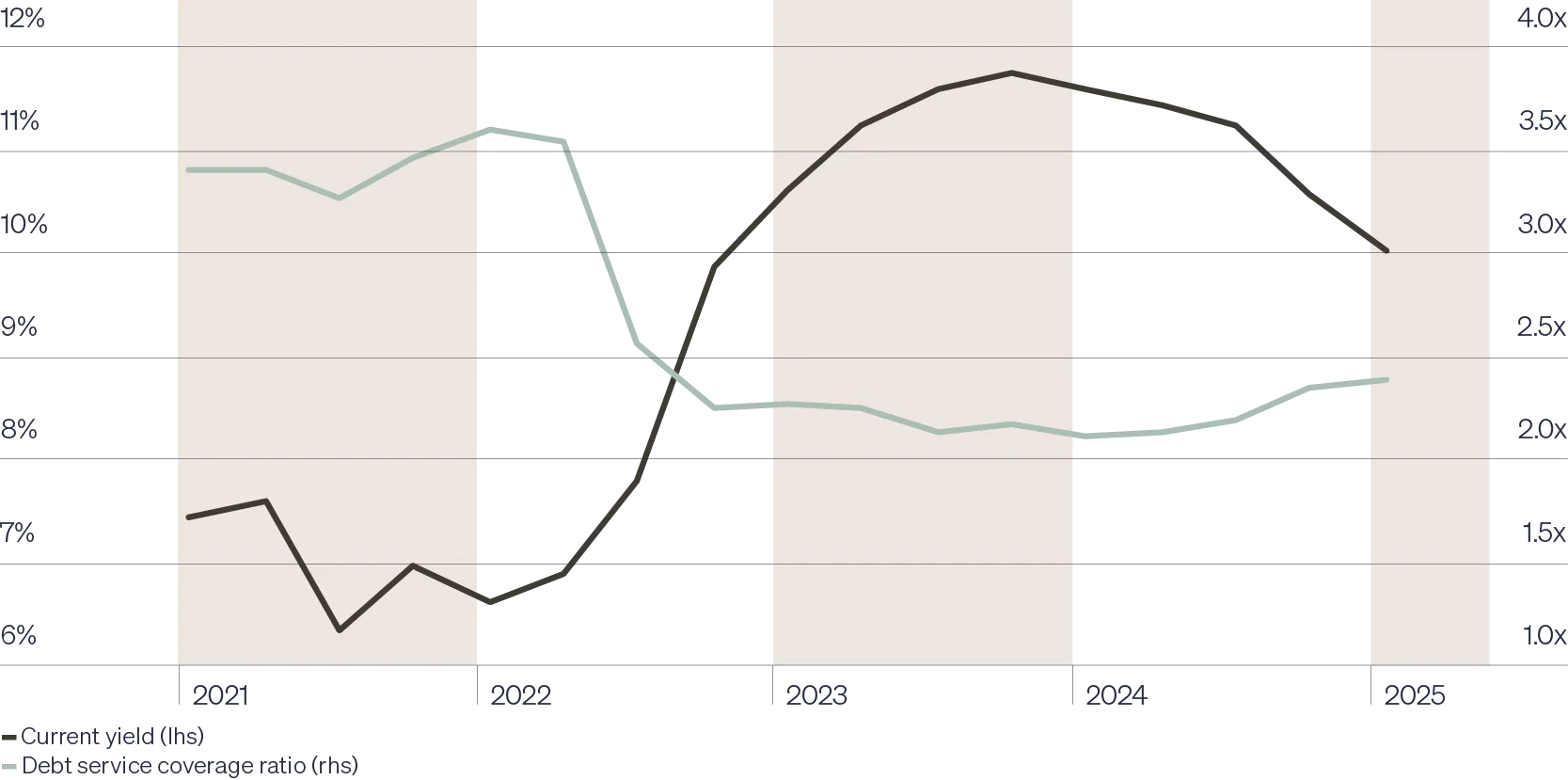

Higher yields, lower margin for error

Senior direct lending yields and borrower interest coverage

Latest data as of May 31, 2025.

Commercial real estate: lender opportunity/borrower strain

The U.S. commercial real estate market has improved markedly from the depths of its correction, but a robust recovery in capital markets activity remains elusive. Just when it appeared the stars were aligning for are bound, policy uncertainty and the attendant macro risks thwarted—or at least delayed—those expectations. As we sit at mid-year 2025, different facets of the market appear to exist in alternative realities: fundamentals are strong, but the construction industry is undergoing recession-like conditions; lenders see significant opportunity, while borrowers remain under strain.

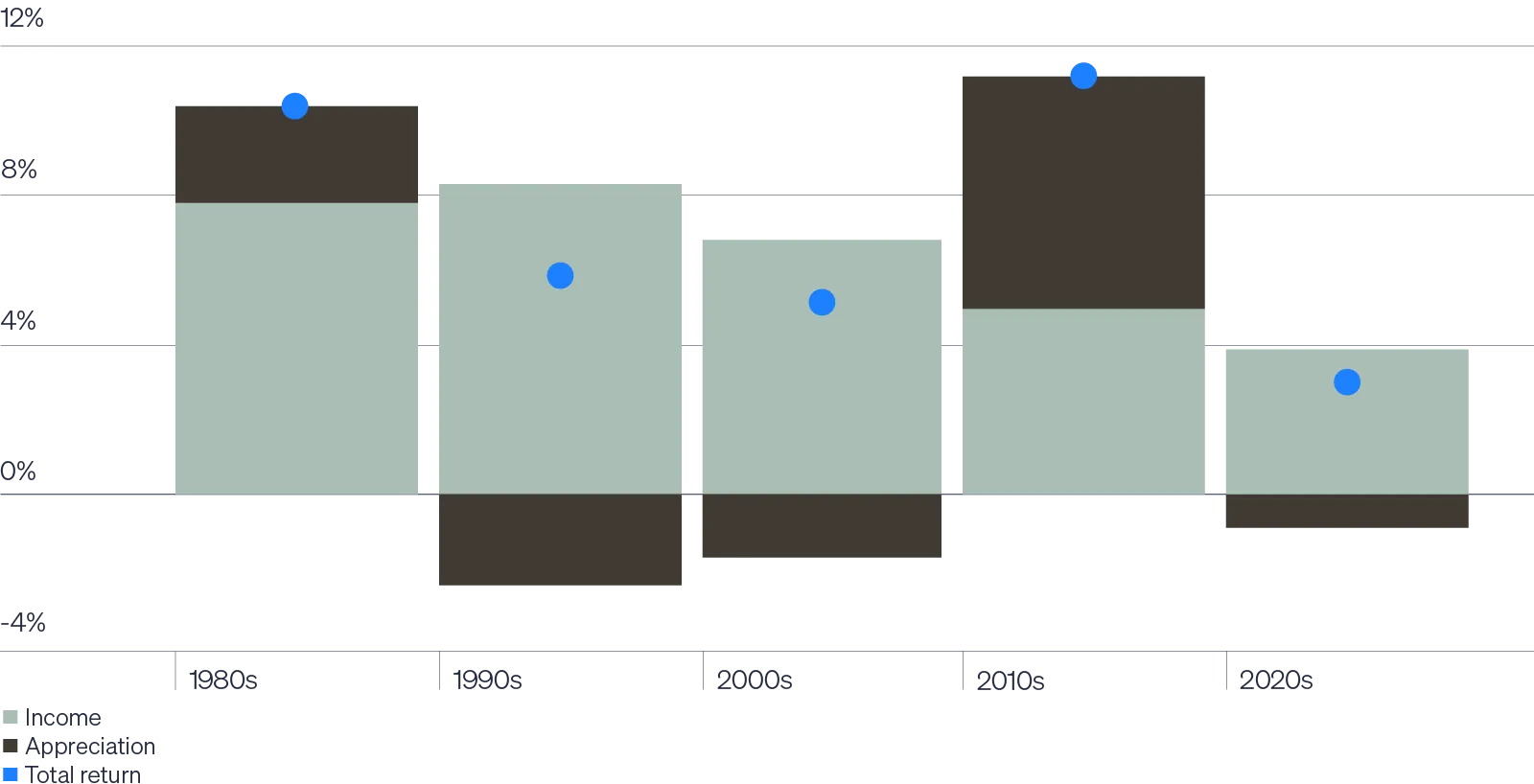

The market is also reckoning with a deeper transformation: durably higher financing costs have fundamentally altered real estate investing. What’s old is new again, as property income will be the primary arbiter of investment performance. This is undermining certain investment strategies, especially those built on high levels of leverage, but also opening up avenues for others. The capital markets malaise of the past few years has delayed much-needed property improvements across geographies and sectors, setting the table for significant opportunities for skilled value-added investors and the lenders that finance them. While we retain a cautious view on risk in commercial real estate, continuing to prefer debt over equity, we see the market continuing to improve—albeit gradually—in the second half.

Breakdown of CRE equity returns by decade