Public equity markets have become increasingly dominated by these AI enablers. As the technology diffuses through the broader economy, the locus of value creation is likely to shift with it—across firms (both tech and non-tech) that deploy AI to unlock productivity gains and operational leverage. With the cost of training frontier models rising sharply and the cost of inference falling rapidly, 2026 represents a natural inflection point for the AI cycle—and for investors’ approach to capturing its next phase.

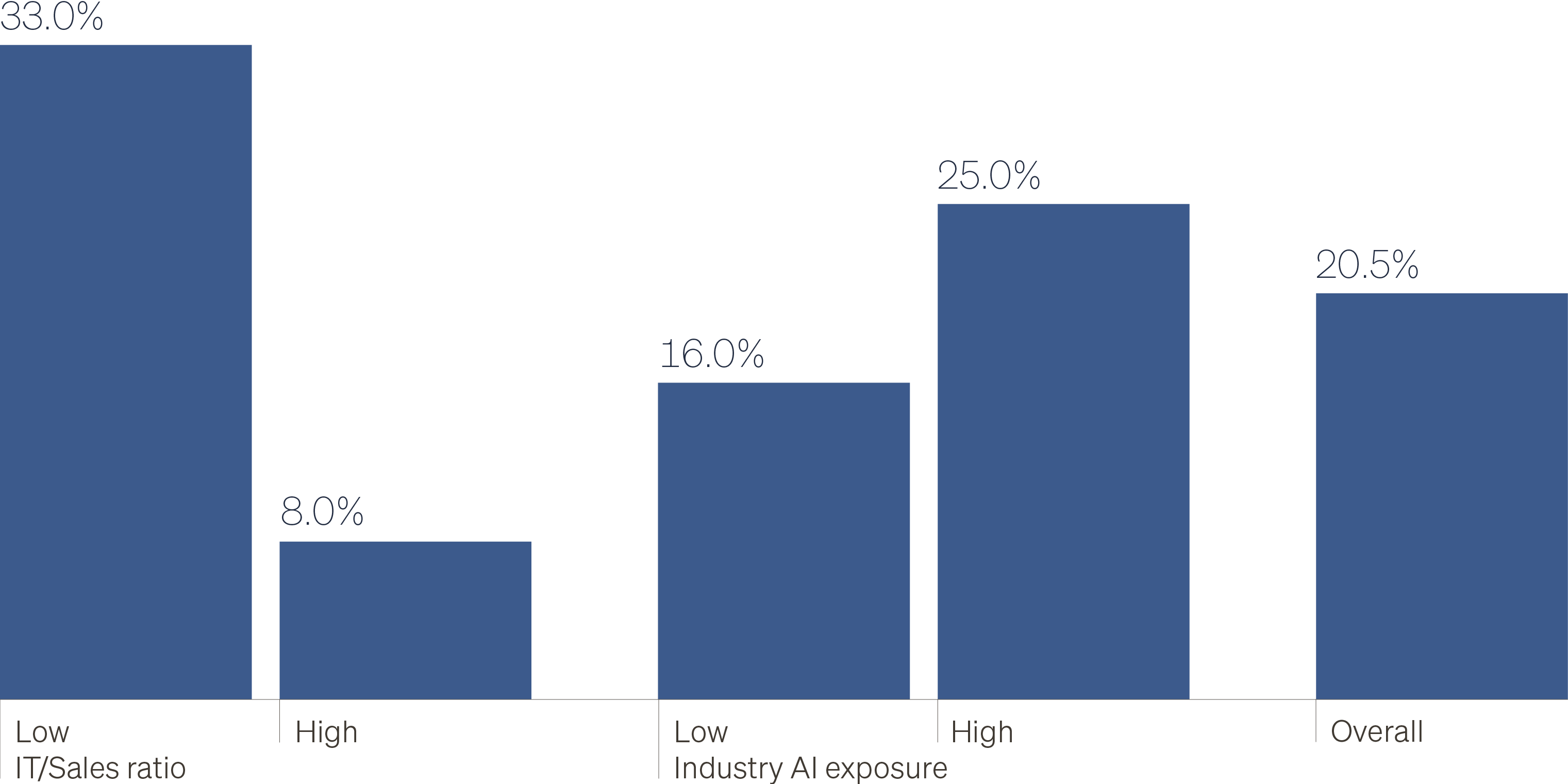

While the first phase of AI-driven value creation largely played out in public markets and a select few privately held labs, private equity buyout is positioned to play a central role in the next phase. Buyout managers have a long, successful track record as technology enablement agents, driving adoption and professionalization—particularly at small and midsize firms that have historically underinvested in IT. Recent academic research underscores this: Firms acquired in buyouts increase IT spending by an average of 21% in the two years post-acquisition relative to comparable non-PE-backed firms, with even larger gains among companies with low initial IT intensity and those in AI-exposed industries.1 Private equity ownership enables rapid investment in technological capabilities across portfolio companies, and AI represents the most powerful catalyst in recent memory.

Relative increase in technology budget in two years post-buyout

Buyout acquirees vs. comparable non-PE-owned firms

AI-driven value creation will unfold over many years, making long-term-hold private equity strategies natural incubators for the technology. Early gains are likely to be incremental, driven primarily by task automation and cost reduction. As AI permeates the enterprise, its impact should progress systematically up the value chain—from task automation and cost reduction, to AI-enabled process redesign, and ultimately to business model transformation and more efficient scale. As this progression unfolds, PE-backed firms stand to benefit not only from sustained capital investment, but also from the shared knowledge, playbooks and infrastructure that experienced PE managers foster across their portfolio companies.

Private equity enablement overlay: Shared knowledge, playbooks and infrastructure across portfolio companies

While AI-driven productivity gains will take time to fully materialize, speed of adoption still matters. Firms that delay integration risk falling behind competitors as capabilities and institutional acumen compound. Although larger firms often have greater resources to deploy, organizational complexity and inertia can slow implementation. Recent evidence supports this dynamic: Wharton’s AI Adoption Report finds that small and midsize firms report faster AI adoption and stronger AI-related ROI. This asymmetry creates a compelling opportunity for private equity—particularly in small and midsize companies where capital, governance and operational expertise can be paired with the agility needed to move quickly.

AI adoption and ROI, by firm size

The capability of AI to automate, augment and in some cases eliminate economically significant functions is accelerating in 2026, well before many enterprises are fully prepared. Public markets, which for three years largely contemplated only AI upside, have begun to discount disruption risks in industries like software and consulting. If these models prove as transformative as many believe, value creation will hinge not just on embracing AI, but on doing so more quickly and effectively than competitors. In that environment, the ability to move fast, deploy operational expertise and distinguish durable beneficiaries from the structurally impaired will define outcomes. We expect AI-enabled operational improvement to be a primary source of alpha, and a defining driver of dispersion, within private equity in the years ahead.